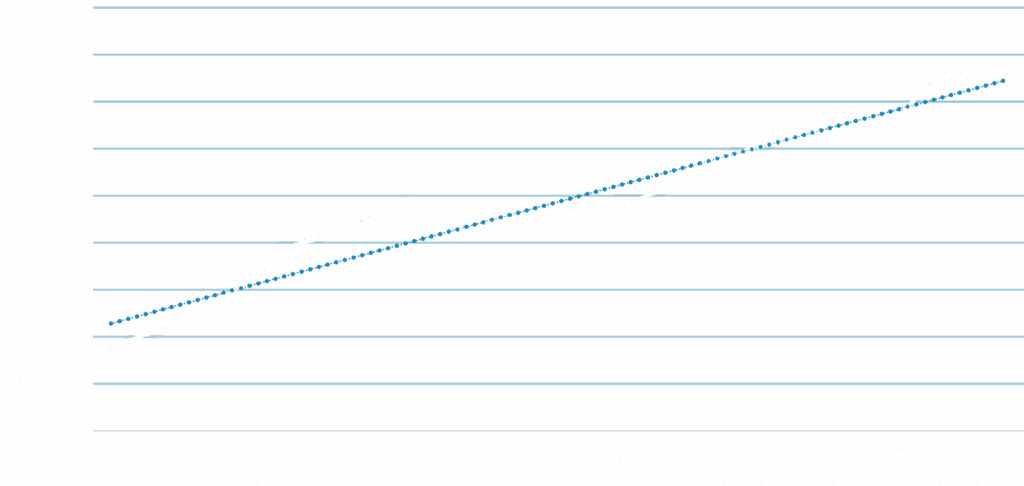

During the last 25 years to March 2024, the average property price in England* rose from circa £70,612 to £305,879 representing a property value increase of approximately 433%.

Transaction data extracted from the Government’s Office for National Statistics (ONS) for England confirms that the average annual compound growth in house prices was approximately 6.0% over the last 25 years.

The graph opposite illustrates that whilst there are irregular cycles of house price growth, the increase is linear over the medium term.

Source: Sales data extracted December 2024 from the ONS for England

|

VPV |

£250,000

|

Investment Price

|

£106,607

|

|

Percentage Share |

100%

|

Discount |

£143,393

|

|

VPV Share

|

£250,000

|

Discount %

|

57%

|

| Term | Future VPV | Reversion Gain | ROI |

|---|---|---|---|

|

5 Years

|

£304,163

|

£197,556

|

185%

|

|

10 Years

|

£370,061

|

£263,454

|

247%

|

|

15 Years

|

£450,236

|

£343,628

|

322%

|

|

20 Years

|

£547,781

|

£441,173

|

414%

|

|

VPV |

£250,000

|

Investment Price

|

£148,326 |

|

Percentage Share |

100%

|

Discount |

£101,674 |

|

VPV Share

|

£250,000

|

Discount %

|

41%

|

| Term | Future VPV | Reversion Gain | ROI |

|---|---|---|---|

|

5 Years

|

£304,163

|

£155,838

|

105%

|

|

10 Years

|

£370,061

|

£221,735

|

149%

|

|

15 Years

|

£450,236

|

£301,910

|

204%

|

|

20 Years

|

£547,781

|

£399,455

|

269%

|

|

VPV |

£250,000

|

Investment Price

|

£89,317

|

|

Percentage Share |

75%

|

Discount |

£98,183

|

|

VPV Share

|

£187,500

|

Discount %

|

52%

|

| Term | Future VPV | Reversion Gain | ROI |

|---|---|---|---|

|

5 Years

|

£228,122

|

£138,805

|

155%

|

|

10 Years

|

£277,546

|

£188,229

|

211%

|

|

15 Years

|

£337,677

|

£248,360

|

278%

|

|

20 Years

|

£410,836

|

£321,519

|

360%

|

In the example below, it would take circa 20 years of house price deflation at 4% per year for the investor to make a gross loss* on their investment.

|

VPV |

£250,000 |

Investment Price

|

£113,185 |

|

Percentage Share |

100%

|

Discount |

£136,815 |

|

VPV Share

|

£250,000

|

Discount %

|

55%

|

| Term | Future VPV | Reversion Gain | ROI |

|---|---|---|---|

|

5 Years

|

£203,843 |

£90,658

|

80% |

|

10 Years

|

£166,208 |

£53,023

|

47% |

|

15 Years

|

£135,522 |

£22,337

|

20%

|

|

20 Years

|

£110,501 |

(£2,684)

|

-2%

|

* Gross loss does not take into consideration sales, legal or any other fees or costs. It also assumes the Life Tenancy has ended.

VPV = Vacant Possession Valuation, PVPV = Proportional Vacant Possession Valuation